Brexit has been a recurring news story in the media for the past few weeks, but the financial markets have been largely unaffected by all the fuss and uncertainty, and at Danske Bank we have maintained an overweight of equities in our portfolios. We still view equities as having a decent return potential in the coming year.

But if Brexit is not a determining factor for your investments, what then should you focus on as an investor? Here, we go through five of the parameters Danske Bank’s strategists weight most heavily – and provide a short assessment of the current state of play:

1. CORPORATE EARNINGS: Better than feared

Equity market growth essentially boils down to how good companies are at earning money. Rising earnings is what justifies rising equity prices, while from an investor perspective an economic upswing is not worth much if companies cannot convert it into increased earnings.

CURRENT STATUS: Looking at the currently ongoing US reporting season, the picture looks pretty solid. So far, many more companies have exceeded analyst earnings expectations than have disappointed, so earnings have been a slap in the face for the worst sceptics. Moreover, earnings have confirmed for us that there is still value to harvest in the equity markets, though we should also point out that analysts have sharply reduced their expectations for 2019 over the past year. Looking ahead, analysts expect average earnings growth of 10% in both 2020 and 2021. These are decent numbers, but subject to great uncertainty – should the economy slow faster or more than expected, these expectations may quickly detach from reality.

SUMMARY: We still expect a level of earnings growth that will support rising equity prices in the coming year.

2. ECONOMIC GROWTH: Upswing with a few cracks appearing

Naturally, we always have a great deal of focus on the overall economic picture – what do the key figures say about Europe, the US and China, which are the world’s most important economies? These data provide an indication of the strength and sustainability of the still ongoing upswing.

CURRENT STATUS: Our overall assessment is that the current upswing still has some time to run – at least 12 months and potentially longer – before we experience an economic downturn. While the global manufacturing sector is faltering, the picture is brighter for the service sector, which fortunately comprises a greater share of the global economy. Here, the confidence indicators (PMI) still point to growth, while consumers are also generally in good shape. Low unemployment and interest rates – and hence low housing costs – are helping to keep consumption buoyant. However, everything is intertwined, so if the manufacturing sector really begins to shed jobs, that will affect consumption and the service sector. Europe is currently the weakest region in terms of growth, pulled lower, in particular, by negative growth in Germany.

The upswing maturing and a subsequent downturn is a completely natural part of the economic cycle. However, while investors fear a repeat of the financial crisis, the most likely outcome is a more normal recession with a slowdown lasting 6-9 months and growth falling a few percentage points, which would give equity markets a greater or lesser shock before the economy slowly begins to pick up again.

SUMMARY: Despite a few cracks appearing, global economic growth continues to support equities overall.

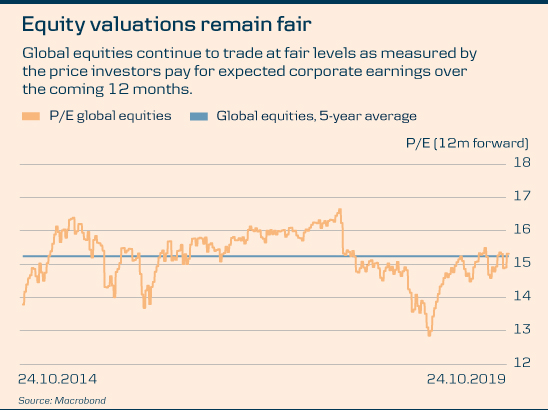

3. VALUATIONS: No alarm bells ringing

Valuations are always a central parameter when we assess the return potential of equities. How much do investors have to pay to get a slice of the company’s earnings? Here, we consider, in particular, P/E (12-month forward), which shows the price (P) per euro of expected earnings (E) in companies over the coming 12 months.

CURRENT STATUS: We assess global equity valuations to be fair at the moment, at around the 5-year average in terms of P/E.

However, those fair valuations are conditional on companies delivering as expected. Should earnings slow, then the reality will suddenly shift, as share prices will have to fall if equities are to trade at around current P/E levels. Here, we should not ignore the possibility that the historically low interest rates and huge liquidity injections of the central banks may have boosted corporate earnings to levels that are not sustainable in the slightly longer term.

SUMMARY: Current equity valuations look reasonable without being particularly cheap.

4. CENTRAL BANKS: An important player

You should never underestimate central banks as a strong driver of how we and many other investors move our money around. Here, we keep a particular eye on inflation and inflation expectations, which are key indicators for central bank monetary policy.

CURRENT STATUS: Central banks have shifted towards more accommodative monetary policies in recent months. This is the case in both Europe and the US and also across a great number of emerging markets – and is unlikely to change any time soon. Since the financial crisis, central banks have pushed interest rates down to historical lows and pumped abnormal amounts of money out into the economy. It is the world’s largest ever economic experiment, and we should be careful to keep that in mind. First, because of the positive effects, which we will naturally try to capitalise on in our investment strategies, but also in terms of any unintended negative consequences in the slightly longer term. While we may not yet have spotted them, we are convinced they exist.

SUMMARY: The accommodative monetary policies of the central banks are supporting the economy and equity markets.

5. POLITICAL RISK: A significant threat

Finally, we have the variable called political risk, which we are spending more time on than previously. We have a new cohort of politicians who are having an impact in areas we have not traditionally been used to. The many political brawls have usually had little effect on the financial markets, but that situation has changed under Donald Trump.

CURRENT STATUS: The trade war between the US and China is a particular problem. Two irreconcilable entities are fighting; for whereas the US is a democracy with presidential elections due in 2020, China’s president, Xi Jinping, is under no democratic pressure to deliver a trade deal, so the trade war could be a brake on the global economy for a long time yet. We may well witness minor easing, but a real resolution would require major backing down by Xi Jinping, and we cannot envisage him bowing. Hence, we have problems seeing how we can move forward before the US potentially elects a new president who can pursue a more stable trade policy – and the longer the trade war draws out, or potentially escalates, the more negative will be the impact on economic growth and corporate earnings.

SUMMARY: Political risk currently poses the greatest headwind for equity markets.

Danske Bank has prepared this material for information purposes only, and it does not constitute investment advice. Always speak to an advisor if you are considering making an investment based on this material to establish whether a particular investment suits your investment profile, including your risk appetite, investment horizon and ability to absorb a loss.